When Should You Review Mortgage Protection? A protection policy records circumstances at a particular moment.

The mortgage had a certain balance. Income came from a particular job. Dependants had specific needs.

Those circumstances can change while the policy remains untouched.

A review does not automatically mean replacing existing cover. It means checking whether the policy still addresses its intended purpose.

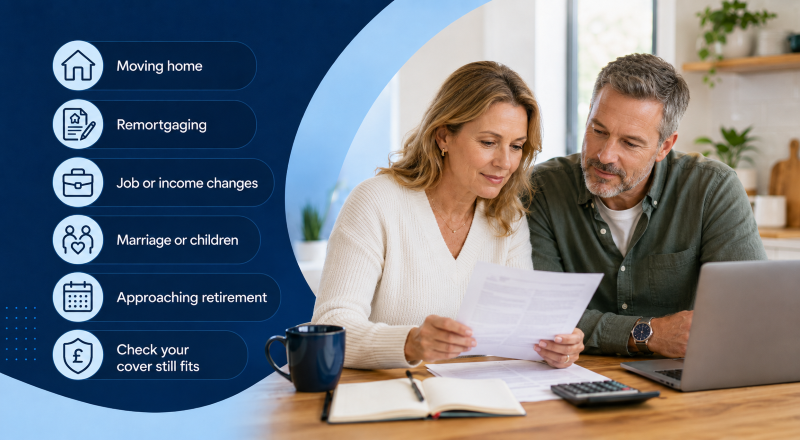

At a Glance

Consider reviewing mortgage protection after:

- Buying or moving home

- Remortgaging

- Borrowing more

- Having a child

- Marriage, divorce or separation

- Changing employment

- Becoming self-employed

- Entering retirement

- Becoming a landlord

- A substantial income change

Never cancel existing cover before replacement insurance is accepted and active.

Why should mortgage protection be reviewed?

A policy may continue exactly as arranged. However, the financial need behind it may have changed.

For example:

- The mortgage balance may have increased

- The mortgage term may have changed

- Household income may rely on a different person

- Employer benefits may have ended

- A new child may depend on the household

- Retirement may now fall within the mortgage term

A review compares the current need with the existing policy.

It does not assume the existing arrangement is unsuitable.

After buying a home

Buying a property is an important point for reviewing insurance.

The purchase may create new responsibilities, including:

- A larger mortgage

- Higher monthly costs

- Buildings insurance requirements

- Shared financial commitments

- Longer travel or childcare costs

- New repair and maintenance expenses

Buildings insurance will usually be required under the mortgage agreement.

Contents insurance and personal protection remain separate considerations.

The residential mortgage guide explains the broader mortgage process.

After moving house

Moving home can change both borrowing and living costs.

A policy based on the previous mortgage might no longer provide enough cover.

Review:

- The new mortgage balance

- The remaining mortgage term

- Any additional borrowing

- Changes to monthly repayments

- New household costs

- Buildings and contents values

- Changes affecting dependants

Porting a mortgage product does not automatically move or adjust every insurance policy.

Some policies can continue unchanged. Others may need updating.

A policy provider should confirm what changes can be made.

After remortgaging

A remortgage can alter the balance, term or repayment structure.

For example, a borrower might:

- Increase borrowing for home improvements

- Consolidate other debts

- Shorten the mortgage term

- Extend repayments into later life

- Change from repayment to interest-only

- Add or remove an applicant

Life cover designed around an earlier repayment mortgage may no longer follow the new balance.

A review can check whether the insured amount and term still correspond with the current mortgage.

Learn how a remortgage may change the underlying borrowing.

After borrowing more

Further borrowing creates a larger financial commitment.

The additional loan may sit on a different interest rate or repayment period.

Existing life cover might only reflect the original mortgage.

Consider:

- The total secured borrowing

- Each loan’s remaining term

- The new monthly commitment

- Whether income protection remains sufficient

- Whether critical illness cover reflects current costs

Increasing an existing policy may require further underwriting.

Age and health changes could affect the available terms or premium.

After marriage or entering a civil partnership

Marriage or a civil partnership can change financial dependency.

One person may contribute more income. Another may provide unpaid childcare or household support.

Both roles have financial value.

A protection review can consider:

- Joint mortgage responsibilities

- Individual and joint policies

- Beneficiary details

- Existing cover

- Wills and trusts

- Dependants from previous relationships

Marriage does not automatically update every policy beneficiary or trust arrangement.

Check the policy documentation and seek legal advice where appropriate.

After separation or divorce

Separation can change ownership, borrowing and financial dependency.

A joint life policy may no longer suit the original purpose.

However, cancelling it immediately could remove valuable cover.

Before making changes, establish:

- Who owns the policy

- Who pays the premium

- Who receives any benefit

- Whether the policy can be separated

- Whether the mortgage is being transferred

- Whether children remain financially dependent

Mortgage, insurance and legal arrangements should be considered together.

After having or adopting a child

A new child can increase the period and amount of financial support required.

Protection might need to account for:

- Childcare

- Housing

- Education

- Household bills

- Reduced working hours

- Unpaid care

- Future family income

Life cover based only on the mortgage may not support these wider needs.

MoneyHelper explains that life insurance can provide financial support for people who depend on the insured person.

After changing employment

A new job may change salary, sick pay and death-in-service benefits.

Employer benefits belong to the employment arrangement. They do not normally follow someone after leaving the organisation.

Check:

- The new salary

- Employer sick pay

- Death-in-service benefits

- Group income protection

- Existing private cover

- Pension benefits

- Notice and probation periods

An increase in salary can also increase household spending.

Therefore, higher earnings do not automatically reduce protection needs.

After becoming self-employed

Self-employment can alter the way income is earned and evidenced.

A self-employed person may have limited sick pay and no employer death-in-service benefit.

Income protection may therefore deserve particular attention.

MoneyHelper notes that self-employed people often consider income protection and critical illness cover because illness could stop them working.

The policy must still reflect:

- Occupation

- Income

- Business structure

- Deferred period

- Savings

- Continuing business expenses

- How the insurer defines incapacity

Company directors should also distinguish personal protection from business protection.

After an income change

A large salary increase or reduction can change the financial calculation.

Higher income might support a larger mortgage and greater household expenditure.

Lower income may make existing premiums difficult to maintain.

Do not cancel protection simply because affordability has become tighter.

Ask whether the policy can be adjusted while retaining valuable terms.

Options may include:

- Reducing the insured amount

- Changing optional benefits

- Reviewing the policy term

- Changing payment frequency

- Removing indexation

- Adjusting the deferred period

Any change should be considered against the resulting reduction in cover.

When approaching retirement

Mortgage terms increasingly extend into later life.

A policy may end before the mortgage does.

Review:

- The mortgage end date

- The protection policy end date

- Expected retirement income

- Pension arrangements

- Future premium affordability

- Savings and investments

- Dependants

- Estate plans

New cover may become more expensive with age. Medical underwriting can also affect the terms.

This makes early review more useful than waiting until a policy expires.

After becoming a landlord

Letting a property changes the insurance risk.

Standard owner-occupier home insurance may not suit a tenanted property.

A landlord should disclose the letting arrangement to the insurer.

Landlord cover may include buildings, landlord contents, liability and selected rental risks.

MoneyHelper states that landlord insurance can include buildings, contents and certain rental-related protection.

Read more about landlord insurance.

Should policies be reviewed after a health change?

A health change does not necessarily require an existing policy to be replaced.

An existing policy may retain terms based on the original application.

A new policy could use current health information and might cost more. It could also include exclusions or be unavailable.

Do not cancel existing protection because circumstances have changed.

First establish whether the current policy remains valid and suitable.

Should you replace an old policy?

Replacement may be appropriate in some circumstances. However, it carries risks.

Before replacing cover, compare:

- Premiums

- Policy definitions

- Exclusions

- Insured amount

- Remaining term

- Guaranteed benefits

- New underwriting requirements

- Waiting periods

- Policy ownership

- Trust arrangements

Older policies may contain definitions or terms worth retaining.

Newer policies may offer broader definitions or additional services.

The publication date alone does not determine which policy is better.

Never cancel cover too early

Do not cancel an existing policy until the replacement has been:

- Fully underwritten

- Formally accepted

- Checked for exclusions

- Confirmed as active

- Reviewed against the existing plan

An application is not the same as active cover.

Cancelling too early can create a period without protection.

A practical review checklist

Ask these questions during a protection review:

- What was this policy originally intended to cover?

- Does that financial need still exist?

- Has the mortgage balance changed?

- Does the policy end before the mortgage?

- Have household dependants changed?

- Has employment protection changed?

- Could premiums remain affordable?

- Are beneficiary details current?

- Is the policy held in trust?

- Would replacement require new underwriting?

- Are exclusions understood?

- Is the insured amount still appropriate?

Protection should follow the need

A mortgage balance changes gradually. Life can change much faster.

A regular review connects the policy to the household it was intended to protect.

It should preserve suitable cover, identify gaps and avoid unnecessary replacement.

Connect Lifetime can help you review how protection relates to your mortgage, income and changing circumstances.

Speak to an adviser before cancelling or replacing existing insurance.

Important information: Insurance is subject to underwriting, eligibility, exclusions and policy terms. Policy changes may affect premiums and benefits.